Markets faced a tug-of-war on Wednesday between lingering optimism that a US-Iran agreement was imminent and a steady drumbeat of contradictory signals that kept traders from fully committing in either direction. WTI crude oil bore the deepest losses of the session as conflicting headlines from Washington and Tehran created whipsaw price action, while equities managed to hold near record territory and the New Zealand dollar emerged as the standout currency mover following a hawkish RBNZ policy statement.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

Promoted: Day traders & Scalpers have better odds of making great decisions if they’re alerted to market catalysts right away, like news of a potential US-Iran agreement, right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

{kind=link}

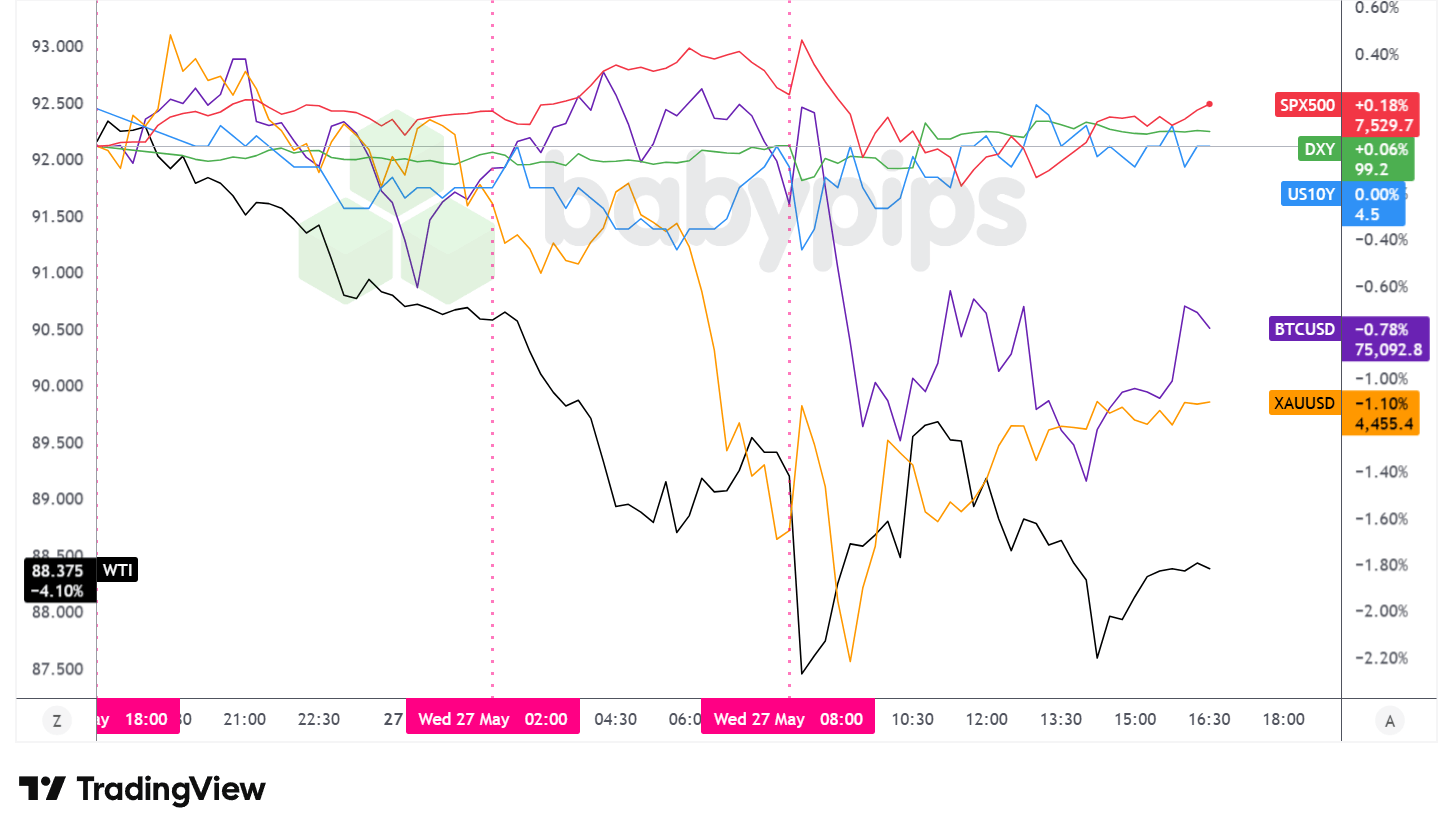

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session featured clear divergence across asset classes, with WTI crude bearing the day’s deepest losses as conflicting signals on a potential US-Iran agreement kept oil traders on edge from the Asian open through the New York close. Equities managed to hold near record territory, gold slid to what sources described as fresh two-month lows, and the dollar ended the day modestly firmer.

WTI crude oil was the session’s hardest-hit asset, settling around $88.40, a decline of roughly 4.12% on the day. Oil had already been drifting steadily lower through the Asian and London sessions as hopes for a deal remained intact but unconfirmed, and selling intensified during the US morning as Trump’s comments cast doubt on near-term progress. The intraday price action was sharp and two-directional, with a brief spike toward the lower end of the day’s range appearing to coincide with the competing Iranian media reports before the White House denial and Trump’s subsequent remarks solidified the bearish tone. An intraday low near $86.75 was established before prices recovered partially into the close.

Gold declined approximately 1.23% to close around $4,452. The precious metal had been under pressure since early in the Asian session, with the move possibly reflecting a broader hawkish repricing in global rate expectations as the RBNZ’s updated OCR projections and BOJ commentary from Governor Ueda both pointed toward tighter monetary conditions ahead. Gold found intraday support near $4,402 before recovering into the US afternoon, though the overall move still represented fresh multi-week lows on the day.

The S&P 500 closed little changed, edging up roughly 0.08% to approximately 7,521. US equities had extended their recent run into the European open, with futures pointing to additional upside, but momentum faded during the US morning as Trump’s Iran comments tempered expectations for an imminent deal. The index pulled back from session highs near 7,554, briefly tested support around 7,499, and ground its way back to roughly flat by the close. Goldman Sachs raised its year-end S&P 500 target to 8,000 during the session, with strategists arguing that AI-driven earnings momentum would support further gains. In after-hours trading, Salesforce issued a tepid revenue outlook while Snowflake raised its sales forecast and announced a commitment to spend an additional $6 billion on Amazon Web Services.

Bitcoin eased approximately 1.39% to around $74,940. The cryptocurrency tracked the mild pullback in risk appetite during the US session without an apparent direct catalyst, posting its losses in a relatively orderly fashion compared to the sharp moves in crude oil.

The US 10-year Treasury yield declined approximately 0.18% to around 4.50%. Yields traded quietly through the Asian and London sessions before easing slightly around the US open. Despite the broadly stronger-than-expected Richmond Fed data and a still-positive weekly ADP employment print, the yield drifted lower on the day, possibly reflecting some safe-haven demand tied to the elevated uncertainty in the Middle East.

Promoted: The Prop Firm Built for Serious Traders.

Don’t let your trading strategy be held back by capital limitations. Alpha Capital Group offers access to simulated funded accounts from $5K to $200K, with entry prices starting as low as $40. They are distinguished by their features, including zero commissions, unlimited trading days during evaluation, and an 80% profit split. Start with a professional-sized account and scale your buying power up to $2M. Join 250K+ traders in 180+ countries today.

Learn more about Alpha Capital Group and current discount codes here!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

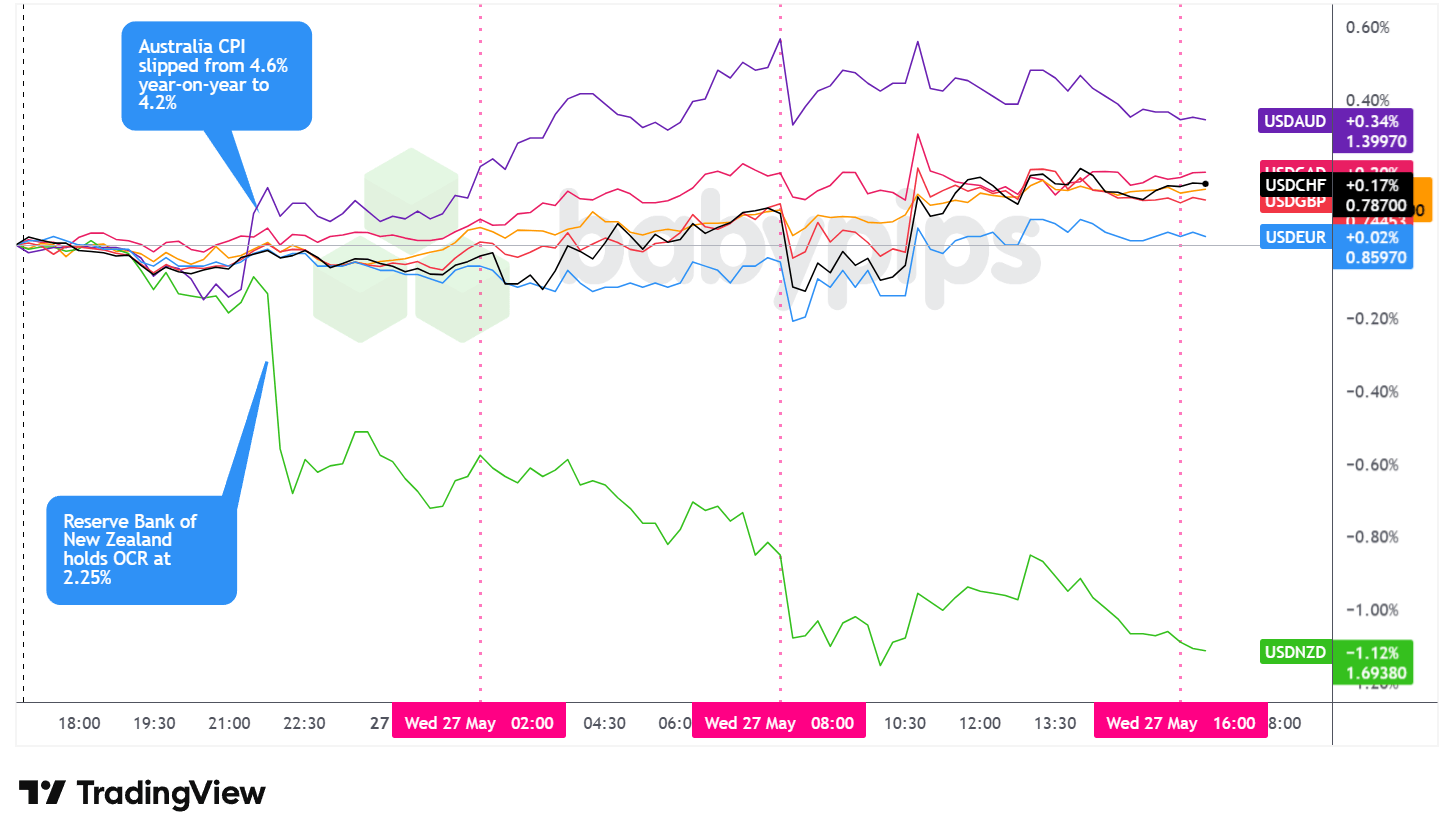

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar traded in a mostly sideways, mixed range during the Asian session, with the Australian dollar and New Zealand dollar serving as the clear standouts due to major domestic catalysts from each country. From the London open onward, the dollar gradually ground higher against most major currencies, with a couple of high-volatility bursts during the US session tied to the competing Iran-related headlines. At the Wednesday close, the dollar posted net gains against all major currencies except the New Zealand dollar, which held onto its RBNZ-driven gains through the final hour of trading.

During the Asian session, the dollar held a relatively quiet and directionless range against the euro, sterling, yen, Swiss franc, and Canadian dollar, with no significant regional catalysts to drive clear momentum in those pairs. AUD/USD came under pressure after the April CPI report printed softer than expected at 4.2% year-on-year versus the 4.6% consensus forecast, with the monthly reading also missing at 0.4% versus a 0.7% forecast. It is worth noting that the trimmed mean measure of core inflation ticked up to 3.4% annually, a 22-month high, suggesting the headline miss may owe in part to temporary factors including a government fuel excise reduction, which leaves the RBA’s June decision genuinely open.

NZD/USD, by contrast, surged sharply as the RBNZ’s Monetary Policy Statement delivered what markets interpreted as a hawkish hold. The OCR was kept at 2.25% by a 3-3 vote resolved by the Governor’s casting vote, but the significantly revised OCR track pointing toward a terminal rate of 3.28% and broad agreement that hikes are coming this year drove meaningful NZD demand. NZD/USD pushed sharply higher during the Asian session and held most of those gains through the remainder of the day.

During the London session, the dollar drifted gradually higher against most majors in a relatively low-volatility grind. The ECB Financial Stability Review was released without new policy signals. France’s Consumer Confidence for May printed below consensus at 82.0 versus a 84.0 forecast, providing a modestly soft European backdrop. Switzerland’s Economic Sentiment Index beat expectations sharply at -11.1 versus a forecast of -24.0, though the franc’s reaction appeared limited relative to the magnitude of the upside surprise. The dollar’s gradual appreciation during this window may have broadly reflected the cautious undertone across risk assets as crude oil continued to slide and gold pressed to fresh lows on the hawkish global central bank repricing narrative.

During the US session, the dollar experienced two notable bouts of elevated volatility. Iranian state TV’s report of a draft MoU possibly corresponded with the sharp intraday dip near the US morning open, one possible explanation for the brief spike lower. The subsequent White House denial and Trump’s pointed dismissal of deal progress appeared to correlate near the dollar recovery.

The Richmond Fed data released during the session was broadly constructive, with the composite manufacturing index surging to 13 versus a forecast of 4 and shipments rising to 16 from a prior reading of -2, while the weekly ADP employment change came in at 35.75k, below the prior 42.25k but still pointing to some labor market resilience. The dollar ultimately held its intraday recovery and closed as a net outperformer, finishing higher against the euro, sterling, Swiss franc, yen, and Canadian dollar while sustaining a loss only against the New Zealand dollar.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- U.K. Car Production for April 2026 at 11:01 pm GMT

- Euro area ECB Lane Speech at 12:00 am GMT

- U.S. Fed Jefferson Speech at 12:00 am GMT

- Australia Household Spending for April 2026 at 1:30 am GMT

- Japan Housing Starts for April 2026 at 5:00 am GMT

- Swiss Non Farm Payrolls for March 31, 2026 at 6:30 am GMT

- ECB Lane Speech at 7:15 am GMT

- ECB President Lagarde Speech at 7:20 am GMT

- Euro area Economic Sentiment for May 2026 at 9:00 am GMT

- European Central Bank Monetary Policy Meeting Accounts at 11:30 am GMT

- U.S. Building Permits Final for April 2026 at 12:10 pm GMT

- Canada Average Weekly Earnings for March 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for May 23, 2026 at 12:30 pm GMT

- U.S. GDP Growth Rate 2nd Est at 12:30 pm GMT

- U.S. Core PCE Price Index for April 2026 at 12:30 pm GMT

- U.S. Durable Goods Orders for April 2026 at 12:30 pm GMT

- U.S. Personal Income & Spending for April 2026 at 12:30 pm GMT

- U.S. Fed Williams Speech at 12:55 pm GMT

- Bank of Canada Financial Stability Report at 2:00 pm GMT

- U.S. New Home Sales for April 2026 at 2:00 pm GMT

- ECB Schnabel Speech at 3:45 pm GMT

- U.S. EIA Crude Oil Stocks Change for May 22, 2026 at 4:00 pm GMT

Thursday brings one of the week’s most data-heavy sessions, with a dense US 12:30 pm GMT window that includes the second estimate of Q1 GDP growth, the Core PCE Price Index for April, Durable Goods Orders, Personal Income and Spending, and the weekly Initial Jobless Claims. The Core PCE print will attract particular attention as the Fed’s preferred inflation gauge, especially given ongoing debate about whether the disinflation trend has stalled.

Earlier in the European session, multiple ECB speakers take the stage including Chief Economist Lane at 7:15 am GMT, President Lagarde at 7:20 am GMT, and Executive Board member Schnabel at 3:45 pm GMT. The ECB’s Monetary Policy Meeting Accounts at 11:30 am GMT may also attract attention for any nuance on the current policy path.

The Bank of England’s Breeden speaks at 8:05 am GMT. Later in the day, the Bank of Canada releases its Financial Stability Report at 2:00 pm GMT, and the EIA crude oil stocks change data at 4:00 pm GMT will be watched closely given the session’s sharp oil price moves.

Stay frosty out there, forex friends!

Wednesday’s market action shows why watching currencies in isolation can leave you blindsided. When crude oil, gold, equities, and the dollar all moved in response to the same geopolitical headlines and central bank repricing, traders who understood how these assets connect had a massive advantage over those watching only the FX chart.

📖 What Is Intermarket Analysis?

Reading this helps you understand how to read stocks, bonds, commodities, and currencies together, why asset class movements confirm or contradict each other, and how to spot divergence before your FX chart tips you off.

And if you’re not a Premium subscriber yet, consider joining to unlock lessons that show you the full picture of how markets work together.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just isolated currency moves, but the intermarket signals that professional traders use to anticipate price action across all asset classes.