")

The U.K.’s April 2026 CPI report came in the middle of one of the year’s most headline-driven weeks, with US-Iran diplomacy whipsawing risk sentiment daily and a newly hawkish Fed adding a secondary layer of dollar volatility on top of the domestic data.

Headline inflation slowed more than expected to 2.8% y/y, reinforcing the case for a cautious BOE, but with geopolitical sentiment doing most of the heavy lifting for price action, the data proved secondary to the broader macro forces already in motion.

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high-quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, check out our BabyPips Premium subscribe page to learn more!

The Setup

What We Were Watching: U.K. Consumer Price Index (April 2026)

- Expectation: Headline CPI to slow down from 3.3% y/y to 3.0% y/y, core CPI to ease from 3.1% y/y to 2.5% y/y

- Data outcome: Headline CPI rose 0.6% month-on-month to bring the annual rate up to 3.8%, core CPI up to 2.8% year-on-year

- Market environment surrounding the event: Risk sentiment was looking fragile leading up to the CPI release, as Trump had declared the US-Iran ceasefire being on “life support” after Tehran rejected the latest peace proposal, while market uncertainty loomed ahead of Kevin Warsh’s confirmation as next Fed Chair

Event Outcome

U.K. headline CPI cooled to 2.8% in April from 3.3%, missing the 3.0% forecast, helped by lower housing and household services costs after the Ofgem energy price cap cut. But analysts warned the drop may be temporary, as higher fuel costs tied to Middle East tensions could push inflation back above 3% later this year.

Sterling dipped after the release but recovered during the European session as traders refocused on sticky underlying pressures. Services inflation cooled sharply, but it remains too hot for the BOE’s comfort.

Key Takeaways:

- Headline CPI: 2.8% y/y (miss vs. 3.0% forecast; prior 3.3%); 0.7% m/m (prior 1.2% m/m in April 2025)

- Core CPI: 2.5% y/y (in-line with 2.5% forecast; down from 3.1%) — lowest reading since July 2021

- Services CPI: 3.2% y/y (down sharply from 4.5% in March) — BOE’s most-watched inflation sub-component

- Goods CPI: 2.4% y/y (up from 2.1%)

- Largest downward driver: Housing and household services, reflecting the Ofgem price cap reduction

- Motor fuel: upward contributor, driven by elevated crude prices linked to the ongoing Middle East conflict

- Base effect caveat: April’s improvement is heavily front-loaded against an elevated April 2025 base (when headline CPI was 3.5% y/y); analysts broadly expect a reversal in May

- BOE watch: Despite the headline drop, wage growth in cash terms continues to run above the BOE’s estimated ~3.25% sustainable threshold, keeping the higher-for-longer narrative intact

Analysts warned that the softer headline may not mark a lasting slowdown in inflation, since temporary and government driven factors did a lot of the heavy lifting. Fuel costs could push CPI back above 3% later this year, with some forecasts seeing a peak near 3.7% by September.

Fundamental Bias Triggered: Bearish GBP

The headline miss was enough to tilt the bias bearish for GBP, as it strengthened the case for a more cautious BOE and kept the door open for more rate cuts later in the year.

The sharp drop in services inflation to 3.2% from 4.5% added to the dovish read, even as analysts flagged base effects and temporary factors behind the move. Still, the data gave traders a clear fundamental reason to sell Sterling and triggered the bearish GBP scenarios laid out in the watchlist.

Promotion: Top-tier catalysts like the U.S. CPI report can trigger emotional execution. TradeZella AI powered journal turns your raw data into a high-performance playbook. Sync your broker, replay your trades bar-by-bar, and use the Playbook Designer to ensure that next time an economic data point surprises the market, you’re executing with clinical precision.

Click on the link to learn more and use code “PIPS20” to save 20% off first purchase!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market and Exogenous Drivers:

US-Iran Escalation and USD Recovery (Monday–Tuesday)

The week kicked off with risk aversion running the show, as confirmed U.S.-Iran military exchanges in the Strait of Hormuz sent traders into the dollar and yen, pushed oil higher, and knocked equities lower. Sentiment found some footing after Trump said he had called off a planned Tuesday strike, giving risk assets room to recover through the London session.

But Tuesday came along and flipped the script. Rising Treasury yields, oil-driven inflation worries, and growing chatter that the Fed may need to shift toward hikes instead of cuts gave the Greenback broad support, handing it its strongest single-day performance of the week.

Iran Deal Optimism Dominates CPI Day (Wednesday)

Trump’s mid-morning comment that U.S. and Iran talks were in their “final stages” knocked the dollar hard during the U.S. session. The 10-year Treasury yield slid from around 4.663 to a low near 4.568 as traders stripped out some of the energy-driven inflation premium that had been sitting in longer-dated rates.

WTI crude also took it on the chin, falling roughly 5.3% on the day. Even the FOMC minutes, which confirmed that most Fed officials had put rate hikes back on the table, couldn’t rescue the Greenback. Markets had already heard that hawkish tune in recent weeks, so Iran deal optimism stayed in the driver’s seat across asset classes.

Conflicting Data and Fading Euphoria (Thursday–Friday)

Thursday served up a messy macro plate. U.S. Manufacturing PMI hit a four-year high, but the Philly Fed headline nearly fell off a cliff, while services PMIs in the eurozone and U.K. both sank deeper into contraction. Mid-session, a report of a final draft Iran deal through Pakistani mediation sparked a sharp jump in stocks and knocked oil lower, but Rubio’s more cautious “some good signs” comment cooled the party pretty quickly.

Friday then delivered the week’s big whiplash. The University of Michigan consumer sentiment index plunged to a record low of 44.8, while longer-term inflation expectations climbed to a seven-month high. That first gave the dollar a quick pop, then dragged it back down as traders focused on the ugly sentiment read. Kevin Warsh’s swearing in as Fed Chair and Waller’s reminder that the next Fed move could just as easily be a hike as a cut helped the Greenback claw back some ground, leaving DXY almost flat for the week.

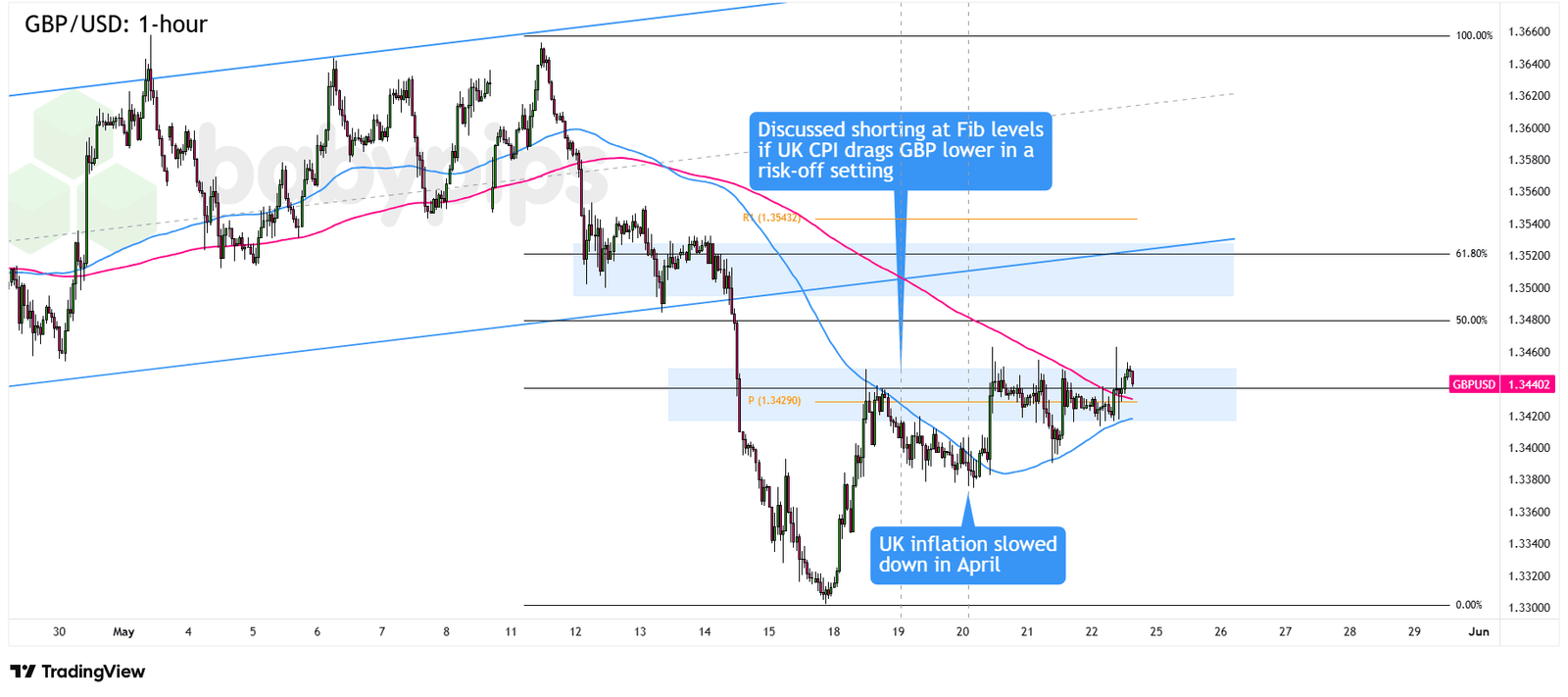

GBP/USD: Bearish GBP Event Outcome + Risk-Off Scenario = Arguably good odds of a net positive outcome

{kind=link}

GBP/USD 1-hour Forex Chart Faster with TradingView

This week, our analysts considered GBP/USD’s potential move lower from below a key Fibonacci and pivot point resistance cluster, with the fundamental case built on hawkish FOMC minutes and a run of U.K. mid-tier data misses keeping the pound on the back foot against the dollar, especially in a risk-averse trading environment.

The early sessions developed largely as the setup anticipated. US-Iran escalation fears kept risk sentiment cautious heading into the week’s primary catalysts, and Sterling underperformed against the dollar during that window. When UK inflation arrived, both headline and core CPI fell short of estimates, removing a key potential upside trigger for the pound. The FOMC minutes reinforced the rate differential story shortly after, confirming that a majority of Fed officials had openly discussed rate hikes — a development that, in quieter conditions, would have been a clean fundamental catalyst for further downside.

The U.K.’s CPI miss, combined with a cautious risk market ahead of the report’s release, made GBP/USD’s setup viable to progress beyond the watchlist stage.

The setup’s clearest test came mid-week. Reports of progress on a US-Iran framework agreement triggered a sharp broad-dollar selloff, lifting GBP/USD alongside the move. However, the recovery stalled below the identified Fibonacci and pivot resistance zone despite the scale of the dollar’s losses — a notable development suggesting that the accumulated weight of the employment miss, the inflation miss, a sharp flash services PMI contraction, lingering political uncertainty, and rising UK gilt yields was still capping upside even as broader sentiment improved.

Sterling bears reasserted themselves when the flash services PMI notably disappointed, pushing GBP/USD back lower. Cautious positioning into the weekend extended the move, leaving the pair below the resistance cluster that had framed the original setup at the week’s close.

Those already short below the resistance cluster ahead of the data events were best placed to weather the mid-week dollar selloff. Those entering on the way down after the services PMI miss were relying on sentiment staying sour into the weekend — and it largely did, but the path required patience.

Promoted: Capitalize on the News Events Without Risking Your Own Funds.

In an economic data surprise, the corresponding currency can swing wildly intraday. Why risk your personal capital during extreme volatility?

Most proprietary firms terminate your evaluation account if you execute a trade during a major macroeconomic release, but FundedNext permits news trading across all models. Test 020your thesis with up to $300,000 in simulated capital, or take advantage of their Free Trial to experience the platform risk-free.

Explore FundedNext and Start Your Free Trial!

Disclosure: We may earn a commission from our partners if you sign up through our links.

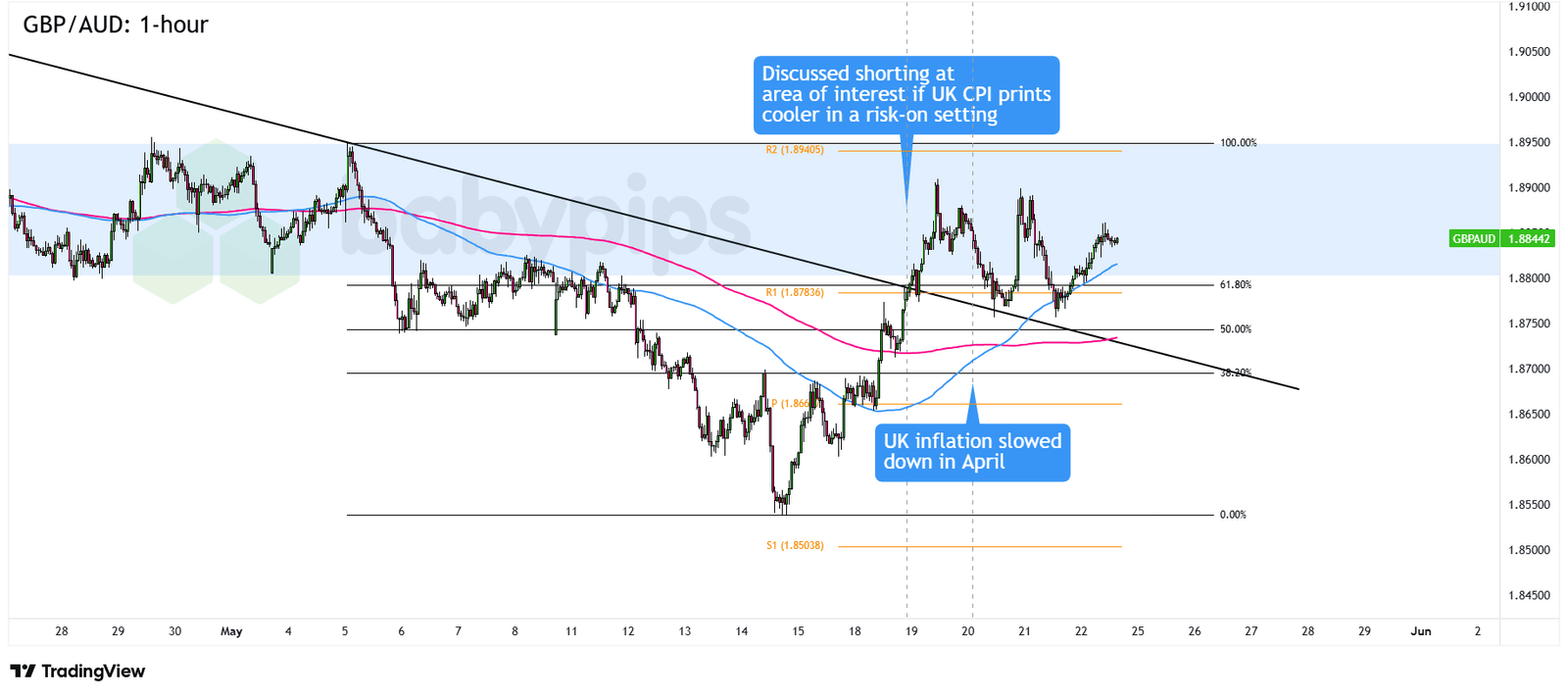

Not Eligible to Move Beyond Watchlist – GBP/AUD & Bullish GBP Setups

GBP/AUD: Bearish GBP Event Outcome + Risk-On Scenario

GBP/AUD 1-hour Forex Chart Faster with TradingView

Our analysts explored a potential move lower based on anticipated pound weakness from U.K. data misses and a softer Australian dollar outlook, with the pending Australian employment report and weak Chinese data forming the key arguments on the AUD side if the U.K.’s CPI printed weak in a risk-friendly setting.

Both headline and core U.K. CPI fell short of estimates, but rather than sparking Sterling weakness in this cross, GBP/AUD moved higher. A broadly disappointing Chinese data release — retail sales and industrial production both missing estimates — had already placed pressure on the Aussie heading into the U.K. inflation print. Market risk sentiment also leaned bearish, with traders focused on a potential escalation in the U.S.-Iran war following social media updates from President Trump.

The result is that, while the major CPI markers missed estimates, concerns over the U.S.-Iran updates kept GBP/AUD’s setup from progressing beyond the watchlist stage.

GBP/AUD continued pushing above the trend line resistance level that had framed the original setup as risk sentiment briefly improved on diplomatic hopes mid-week. The Aussie lost further momentum later in the week as those hopes faded and the Chinese data headwinds reasserted themselves across AUD crosses. The pair held above trend line resistance through the back half of the week, with AUD softness doing the heavier lifting in driving the move rather than any independent sterling catalyst.

The week closed with GBP/AUD above the level the original short idea had required. Those who had anticipated Aussie softness from the Chinese data dump rather than waiting for the U.K. CPI trigger were best placed to ride the move above trend line resistance. Those looking for a clean short entry found the trigger conditions had shifted by the time the week’s key events had passed.

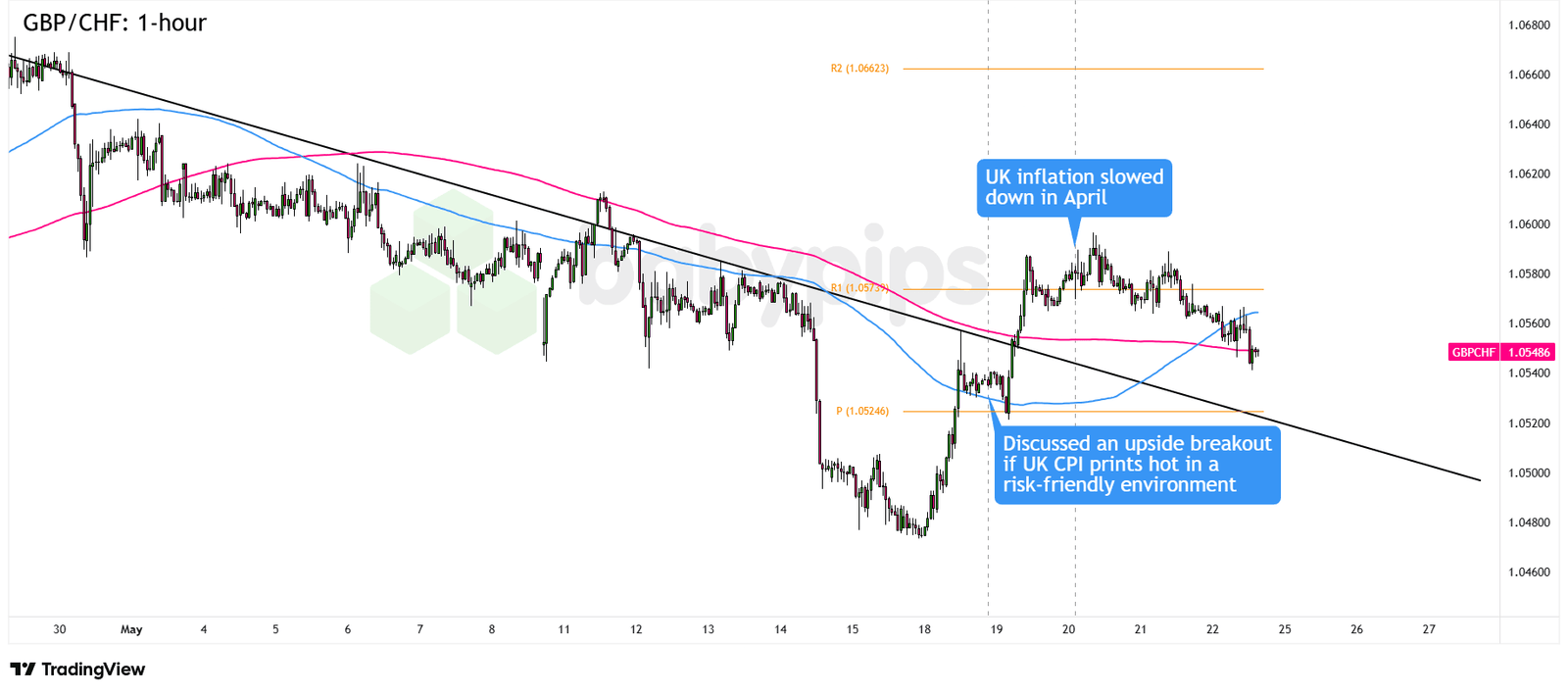

GBP/CHF: Bullish GBP Event Outcome + Risk-On Scenario

GBP/CHF 1-hour Forex Chart Faster with TradingView

Our GBP/CHF watchlist idea focused on the bullish flag pattern forming just below the falling trend line on its hourly time frame, projecting a potential break higher and reversal in the event the U.K. CPI comes in hotter than expected in a risk-friendly scenario.

Because both headline and core CPI readings fell short of expectations, the fundamental trigger for this setup was not activated. In addition, risk sentiment leaned mostly negative around the CPI release as geopolitical tensions were heightened when Trump said the US-Iran ceasefire was on “life support” and the hawkish Fed narrative came back in play.

The pair had already broken above the trend line resistance zone to test R1 (1.0574) ahead of the target event, as the U.K. jobs report released the day before showed some green shoots in wage growth and positive revisions to previous data.

The actual inflation miss merely spurred a quick dip while the pair held on to R1 and the 1.05800 major psychological handle midweek, as risk appeared to return when diplomatic hopes return on Trump’s remarks that US-Iran negotiations are in their “final stages.”

Pound bears managed to regain the upper hand when the U.K. flash services PMI notably disappointed, taking GBP/CHF back below the 1.05700 mark on Thursday, while souring sentiment and cautious positioning into the weekend extended the slump below 1.05600.

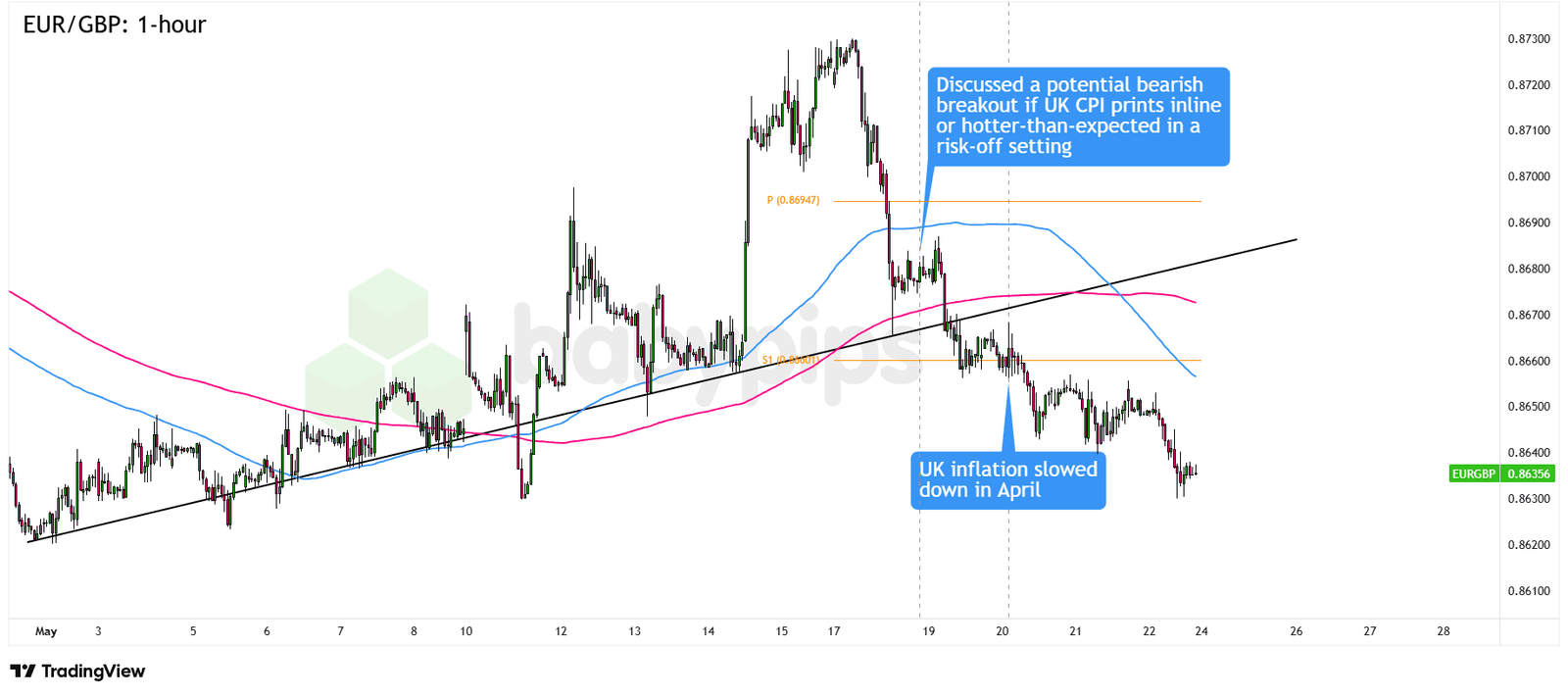

EUR/GBP: Bullish GBP Event Outcome + Risk-Off Scenario

EUR/GBP 1-hour Forex Chart Faster with TradingView

This watchlist idea looked into a potential EUR/GBP rising trend line breakdown and resulting downtrend in the event that the U.K. CPI beats estimates in a risk-off scenario.

Though the pair already showed some bearish momentum leading up to the target event, as risk aversion picked up on prolonged geopolitical uncertainty and the U.K. employment report showed signs of life in the jobs market, the actual CPI numbers came in below estimates and invalidated the fundamental bias of this setup.

Still, the downbeat U.K. inflation figures caused a meager pop higher for the pair, which fought but failed to hold on to the S1 support. Further downside momentum followed as flash eurozone PMI readings turned out mostly in contractionary territory while the U.K. manufacturing sector displayed resilience, taking EUR/GBP down to the next support zone at the .8650 minor psychological mark.

Another break lower took place towards the end of the week, despite downbeat U.K. retail sales data, as deteriorating eurozone business activity and cautious positioning into the weekend kept the shared currency on the back foot.

The Verdict

GBP/USD ended the week below the identified Fibonacci and pivot resistance cluster, and the weekly recap had the right read: the pound was carrying too many headwinds for a mid-week geopolitical relief rally to fully reverse the damage.

The fundamental triggers largely delivered. Both headline and core CPI missed estimates, the flash services PMI disappointed sharply, and the FOMC minutes confirmed that a majority of Fed officials had openly discussed rate hikes — a meaningful shift in the rate differential story that kept the dollar supported even through periods of geopolitical optimism. None of these individually represented a dramatic policy shift, but together they kept a ceiling on any sustained sterling recovery.

The week’s most direct test of the setup came mid-session Wednesday. Iran deal optimism triggered one of the sharpest broad-dollar selloffs of the conflict regime, lifting GBP/USD off its lows and driving it straight into the resistance zone. The critical observation is that the recovery stalled there — below the Fibonacci and pivot cluster — even at the height of the dollar’s weakness. In other words, the setup’s structural argument held under the most adverse conditions the week produced.

The services PMI miss then provided the push that extended the move lower into the close. Cautious weekend positioning did the rest, leaving the technical picture largely intact by Friday.

Overall, we’d rate this GBP/USD discussion as neutral for a net positive outcome. The direction was right, the key triggers fired, and the technical structure held through a mid-week reversal that could have broken it. The main complication was timing — the Iran-driven dollar selloff created a window of significant adverse pressure that required patience to sit through.

Traders already positioned ahead of the FOMC and CPI events were best placed to hold through that volatility. Those entering after the services PMI miss were stepping in after the week’s most difficult passage had already passed.

Key Takeaways:

A Soft CPI Print Doesn’t Always Break a Currency When the Central Bank Pushes Back

April’s inflation miss pointed toward a more dovish BOE path, but sterling absorbed the data without meaningful net losses. Multiple BOE speakers injected hawkish caveats on the same day, flagging second-half inflation risks and warning of forceful action if Middle East energy disruptions persist, which anchored GBP against clean breakdown attempts.

Application: When a central bank speaks with nuance on the same day a soft print crosses the wire, the policy offset can neutralize what looked like a straightforward directional catalyst.

Exogenous Drivers Can Override Domestic Catalysts Entirely

Sterling ended the week as the best-performing major currency, despite a CPI miss, mixed labor data, a PMI Services collapse, and disappointing retail sales. That outcome was arguably attributable to the shifting geopolitical mood around US-Iran diplomacy.

Application: When a major geopolitical catalyst is running in parallel with a scheduled data event, assign meaningful probability weight to the scenario where the data is simply absorbed without lasting directional impact because sentiment flows may do the steering regardless.

This U.K. CPI recap highlights how a softer-than-expected inflation print failed to break GBP lower, in part because BOE speakers pushed back on the same day. If the interaction between data outcomes and central bank communication is unfamiliar territory, Premium members can read our lesson:

📖 How to Trade Central Bank Decisions Using Market Expectations

Reading this helps you understand what “priced in” really means, the four scenarios every trader must prepare for around a major data or policy event, and why central bank tone on the day can neutralize what looks like a clear directional catalyst.