Wednesday’s session pivoted on two forces pointing in sharply different directions. President Trump’s assertion that US-Iran peace negotiations are approaching resolution sent crude oil tumbling below $100 per barrel and lifted equities and risk-sensitive currencies, while minutes from the Federal Reserve’s April 28–29 meeting confirmed a plainly hawkish internal debate, with a majority of officials warning that rate hikes may become necessary if inflation remains persistently above target.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- U.S. API Crude Oil Stock Change for May 15, 2026: -9.1M (-2.19M previous)

- Japan Reuters Tankan Index for May 2026: 8.0 (8.0 forecast; 7.0 previous)

- Germany PPI for April 2026: 1.7% y/y (1.6% y/y forecast; -0.2% y/y previous)

-

U.K. CPI Growth Rate for April 2026: 2.8% y/y (3.0% y/y forecast; 3.3% y/y previous)

- U.K. Core Inflation Rate for April 2026: 2.5% y/y (2.7% y/y forecast; 3.1% y/y previous)

- Euro area Inflation Rate Final for April 2026: 3.0% y/y (3.0% y/y forecast; 2.6% y/y previous)

- Euro area Core Inflation Rate Final for April 2026: 2.2% y/y (2.2% y/y forecast; 2.3% y/y previous)

- U.S. MBA 30-Year Mortgage Rate for May 15, 2026: 6.56% (6.46% previous)

- U.S. MBA Mortgage Applications for May 15, 2026: -2.3% (-1.7% previous)

- U.S. EIA Crude Oil Stocks Change for May 15, 2026: -7.86M (-4.31M previous)

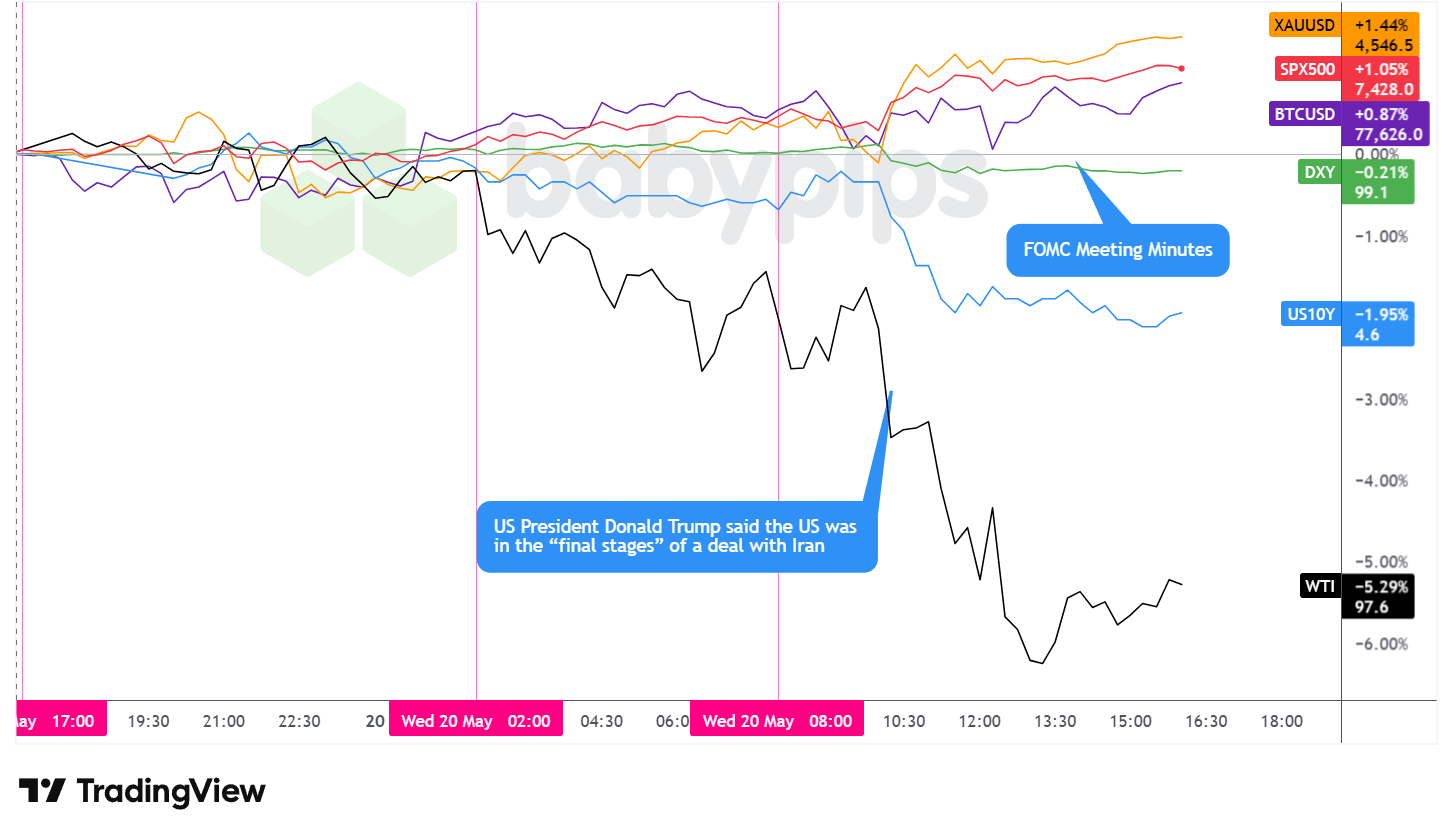

- FOMC Meeting Minutes: The Fed held rates steady at 3½–3¾%, with nearly unanimous support, as elevated inflation (PCE at 3.5% in March, driven largely by Middle East conflict-related energy prices) outweighed a softening labor market. A majority of participants flagged that policy firming could become appropriate if inflation continues running persistently above 2%, and many wanted to remove easing-bias language from the statement.

- During the Wednesday US session, the US President Donald Trump said the US was in the “final stages” of a deal with Iran

- Nvidia reported fiscal first-quarter results after the Wednesday close: Revenue of $81.62B vs $78.86 B; Earnings per share at $1.87

Promoted: Day traders & Scalpers have better odds of making great decisions if they’re alerted to market catalysts right away, like news of a potential US-Iran agreement, right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

{kind=link}

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session was defined by two headline-driven inflection points: President Trump’s mid-morning statement that US-Iran negotiations were in the “final stages,” which triggered a sharp repricing across energy, equities, and rates, and the afternoon release of hawkish FOMC minutes from the April 28-29 meeting that confirmed a majority of Fed officials have put rate hikes back on the table.

WTI crude oil suffered the session’s most dramatic move, falling roughly 5.29% to near $97.60 per barrel. The selloff had been building through the overnight and London sessions, with oil declining gradually before accelerating sharply around mid-morning in New York following Trump’s Iran comments. The intraday low came near $96.20 before a partial recovery through the afternoon. The EIA crude inventory report, released around the same time as Trump’s remarks, showed a draw of 7.86 million barrels for the week ended May 15, larger than the prior week’s 4.31 million barrel draw. That figure would ordinarily have been oil-supportive, but the diplomatic headlines appeared to dominate the price action entirely, with markets pricing in the possibility of resumed Hormuz transit and a gradual normalization of Middle East supply.

The S&P 500 gained roughly 1.05%, closing near 7,428 and halting a three-day losing streak. The index had drifted gradually higher through the European morning before making a sharp leg up around the time of Trump’s Iran comments, briefly touching a high near 7,437. It then settled into a range just above the prior day’s high area near 7,418, absorbing the FOMC minutes without giving back meaningful ground. Nvidia’s earnings, expected after the close, provided an additional layer of focus for equity traders given the stock’s outsized influence on the broader index.

Gold posted the session’s strongest relative performance, climbing roughly 1.44% to near $4,546 per ounce. The precious metal had been under pressure during the Asian session, sliding toward the $4,453 area, before recovering through London trade and then surging alongside the broader shift in risk sentiment during New York hours. Gold touched a session high near $4,553 before consolidating and continuing to trend higher through the afternoon. Its advance alongside equities may reflect that the FOMC minutes’ hawkish tone sustained safe-haven interest even as risk assets rallied — one possible interpretation being that markets viewed the Iran deal as not yet certain enough to fully unwind inflation hedges.

Bitcoin posted modest gains of roughly 0.87%, trading near $77,626. The cryptocurrency pushed higher during early Asian trade before ranging broadly through the session, dipping briefly around the US open before recovering to close above the prior day’s high area. Its relatively contained move compared to the larger swings in oil and equities possibly reflected consolidation within a narrower recent range.

The 10-year US Treasury yield declined roughly 1.95%, settling near 4.60%. Yields had been elevated during the Asian session before beginning a gradual descent through London. The drop accelerated sharply around mid-morning New York time, correlating with Trump’s Iran comments and the associated repricing of near-term energy-driven inflation risk, with the yield sliding from near 4.663 to a low near 4.568. Yields continued drifting lower through the afternoon even after the FOMC minutes reinforced the possibility of rate hikes, possibly suggesting the market’s dominant read was that a diplomatic resolution to the conflict, if realized, would remove the primary engine of near-term inflation rather than implying an imminent tightening cycle.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $15, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

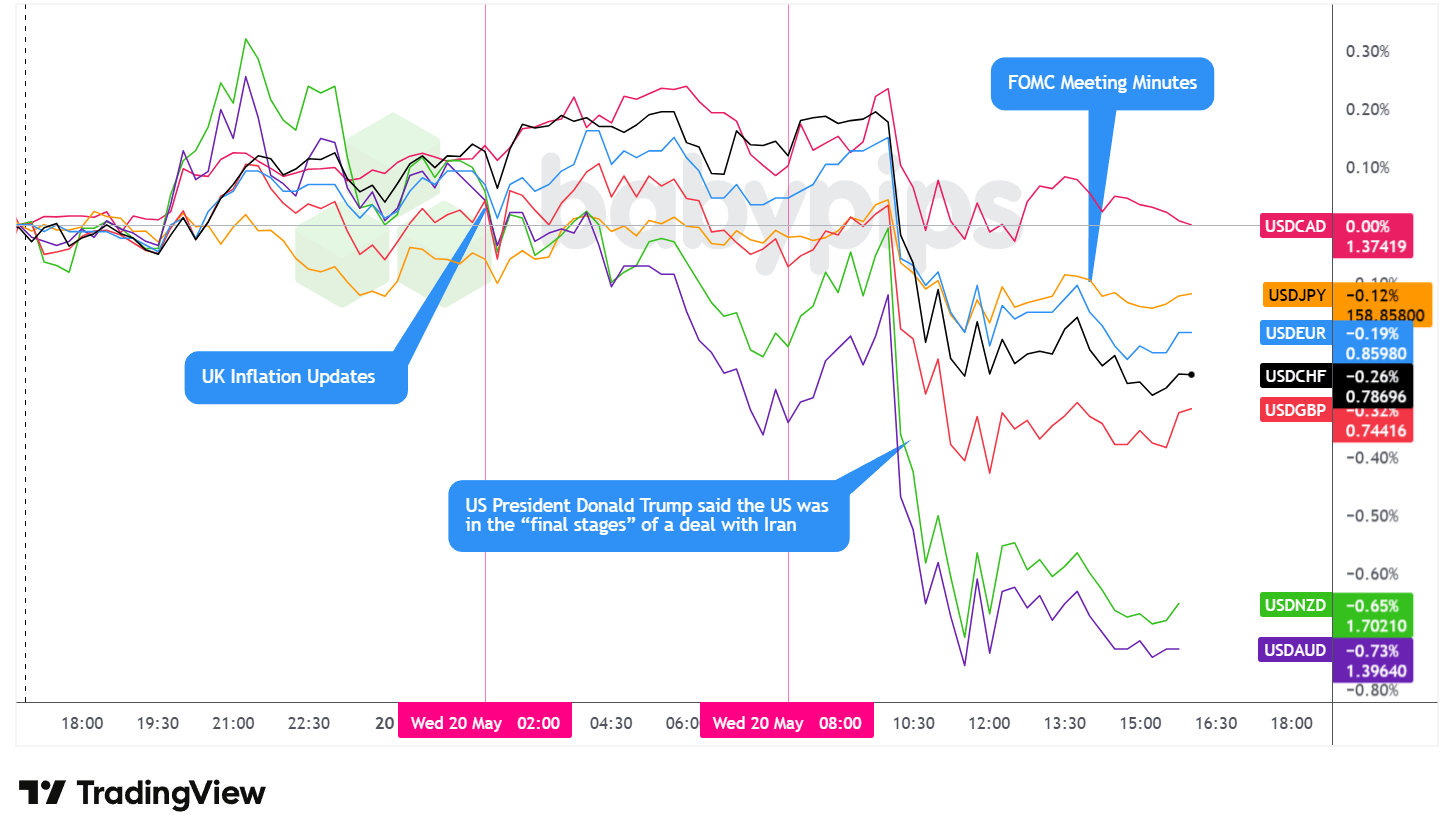

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

The US dollar closed Wednesday as arguably one of the worst performers among the major currencies, with most of the damage concentrated in the US session as diplomatic headlines and an overall risk-on tone combined to pressure the greenback broadly.

During the Asian session, the dollar traded choppy and sideways with an arguably net bullish lean. No meaningful regional catalysts drove directional conviction. China’s decision to hold its one-year and five-year loan prime rates unchanged for a twelfth consecutive month came in exactly as expected and generated little market reaction.

The London session opened with the dollar continuing its broadly sideways, choppy behavior. The headline economic release was the UK April inflation package, which came in below expectations across the key measures: headline CPI printed at 2.8% y/y against a 3.0% forecast and a prior reading of 3.3%, while the core rate fell to 2.5% y/y versus 2.7% expected. Despite the softer UK consumer inflation data, the dollar did not strengthen materially against the pound, possibly because the UK PPI figures — which beat expectations on the output, core output, and input measures — provided a more hawkish counterpoint to the CPI softness.

Euro area final CPI for April confirmed the headline at 3.0% y/y, picking up from 2.6% in the prior month, adding to a backdrop of elevated European inflation that kept ECB rate hike speculation active. By the approach of the New York open, the dollar had begun dipping more noticeably against most pairs.

The US session opened with the dollar attempting a brief and modest recovery, but the rebound proved short-lived. President Trump’s mid-morning statement that US-Iran talks were in the “final stages” triggered a sharp, broad-based dollar selloff that deepened through the London close.

The FOMC minutes, released around 2:00 p.m. ET, confirmed the hawkish shift at the April meeting, with a majority of officials signaling openness to rate hikes if inflation runs persistently above 2%. The minutes did not reverse the dollar’s decline, possibly because the degree of Fed hawkishness had already been well-telegraphed in recent weeks, leaving the Iran deal optimism as the dominant driver. After the London close, the dollar stabilized and traded mostly choppy and sideways for the remainder of the session.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

Most trading mistakes aren’t technical—they’re psychological. In the classic “Trading in the Zone” by Mark Douglas (⭐ 4.7★ | 10,000+ reviews on Amazon), you’ll learn how to master the probabilistic thinking and emotional discipline mentioned in today’s article. If you struggle with hesitation or breaking your rules, this is your manual for consistent execution.

Click on the link to learn more about “Trading in the Zone” by Mark Douglas!

Disclosure: To help support our content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Balance of Trade for April 2026 at 10:45 pm GMT

- Australia S&P Global Manufacturing & Services PMI Flash for May 2026 at 11:00 pm GMT

- Japan Balance of Trade for April 2026 at 11:50 pm GMT

- Japan Machinery Orders for March 2026 at 11:50 pm GMT

- Japan S&P Global Manufacturing & Services PMI Flash for May 2026 at 12:30 am GMT

- Australia Consumer Inflation Expectations for May 2026

- Australia Westpac Leading Index for April 2026

- Australia Employment Situation update for April 2026 at 1:30 am GMT

- Bank of Japan Koeda Speech at 1:30 am GMT

- New Zealand Credit Card Spending for April 2026 at 3:00 am GMT

- Swiss Industrial Production for March 31, 2026 at 6:30 am GMT

- Euro area S&P Global Manufacturing & Services PMI Flash for May 2026 at 8:00 am GMT

- U.K. S&P Global Manufacturing & Services PMI Flash for May 2026 at 8:30 am GMT

- Euro area Labour Cost Index Flash for March 31, 2026 at 9:00 am GMT

- U.K. CBI Industrial Trends Orders for May 2026 at 10:00 am GMT

- U.S. Building Permits & Housing Starts for April 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for May 16, 2026 at 12:30 pm GMT

- U.S. Philadelphia Fed Manufacturing Index for May 2026 at 12:30 pm GMT

- Bank of England Taylor Speech at 1:00 pm GMT

- U.S. S&P Global Manufacturing & Services PMI Flash for May 2026 at 1:45 pm GMT

- Euro area Consumer Confidence Flash for May 2026 at 2:00 pm GMT

- U.S. Kansas Fed Manufacturing Index for May 2026 at 3:00 pm GMT

Thursday brings a dense lineup of flash PMI readings from Australia, Japan, the eurozone, the UK, and the US, offering the first May snapshot of business activity momentum across major economies.

The Australia employment report at 1:30 am GMT will draw particular attention given the Australian dollar’s outperformance on Wednesday, with any softness in jobs data potentially testing whether AUD’s gains can hold.

The BOJ’s Koeda speech and the BOE’s Taylor speech could attract scrutiny given ongoing yen intervention sensitivity and the BOE’s delicate positioning following Wednesday’s softer-than-expected UK CPI print.

In the US session, weekly initial jobless claims and the Philadelphia Fed Manufacturing Index at 12:30 pm GMT arrive against a backdrop of heightened Fed inflation vigilance reinforced by Wednesday’s minutes, with markets sensitive to any signals of labor market deterioration or economic cooling. The flash US PMIs at 1:45 pm GMT will add further color on whether underlying growth momentum is holding or beginning to soften under the weight of elevated energy costs.

Stay frosty out there, forex friends!

Wednesday’s session showed exactly how the bond market, equity indices, oil prices, and geopolitical risk all moved together to shape currency flows. But most traders watch these markets separately, missing the connections that predicted the dollar’s move before it happened. Premium members can read our lesson:

📖 What Is Intermarket Analysis?

Reading this helps you understand how Treasury yields affect currency movements, why rising bond yields supported the dollar while pressuring equities and gold, and how to read stocks, bonds, commodities, and currencies together so you see the full picture before placing any trade.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just how individual markets move, but how they drive each other and shape currency flows before price action even appears on your chart.