A sharp escalation in US-Iran hostilities overnight rattled energy markets and risk sentiment on Wednesday, driving crude oil firmly higher and snapping the S&P 500’s nine-session winning streak.

A simultaneous wave of stronger-than-expected US economic releases, including a substantially above-forecast ADP employment report and a robust ISM Services PMI, reinforced the possibility that the Federal Reserve may shift toward a more hawkish policy stance, pushing Treasury yields and the dollar broadly higher while weighing on gold and Bitcoin.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Japan S&P Global Services PMI Final for May 2026: 50.0 (50.0 forecast; 51.0 previous)

- Australia GDP Growth Rate for Q1 2026: 0.3% q/q (0.5% q/q forecast; 0.8% q/q previous)

- China RatingDog Services PMI for May 2026: 54.4 (52.5 forecast; 52.6 previous)

- Germany S&P Global Services PMI Final for May 2026: 48.1 (47.8 forecast; 46.9 previous)

- Euro area S&P Global Services PMI Final for May 2026: 47.7 (46.4 forecast; 47.6 previous)

- U.K. S&P Global Services PMI Final for May 2026: 49.3 (47.9 forecast; 52.7 previous)

- Euro area PPI for April 2026: 0.6% m/m (1.9% m/m forecast; 3.4% m/m previous)

- Germany New Car Registrations for May 2026: 0.1% y/y (4.2% y/y forecast; 2.7% y/y previous)

- U.S. MBA 30-Year Mortgage Rate for May 29, 2026: 6.57% (6.65% previous)

- MBA Mortgage Applications for May 29, 2026: -2.5% (-8.5% previous)

- ADP National Employment Report for May 2026: 122.0k (75.0k forecast; 109.0k previous)

- Canada Labor Productivity for Q1 2026: -0.5% q/q (0.5% q/q forecast; -0.1% q/q previous)

- Canada S&P Global Services PMI for May 2026: 50.6 (49.6 forecast; 49.2 previous)

- U.S. S&P Global Services PMI Final for May 2026: 50.7 (50.9 forecast; 51.0 previous)

- ISM Services PMI for May 2026: 54.5 (53.0 forecast; 53.6 previous)

- U.S. Factory Orders for April 2026: 4.8% m/m (2.7% m/m forecast; 1.5% m/m previous)

- U.S. EIA Crude Oil Stocks Change for May 29, 2026: -7.97M (-3.33M previous)

Promotion: TradeZella is the top journaling app in the industry, and its new AI trading partner feature can break down and analyze your trades & build a game plan, freeing up time and energy to focus on the next moves!

Start Your Trading Journey with Tradezella & use code “PIPS20” for 20% off your first purchase!

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

{kind=link}

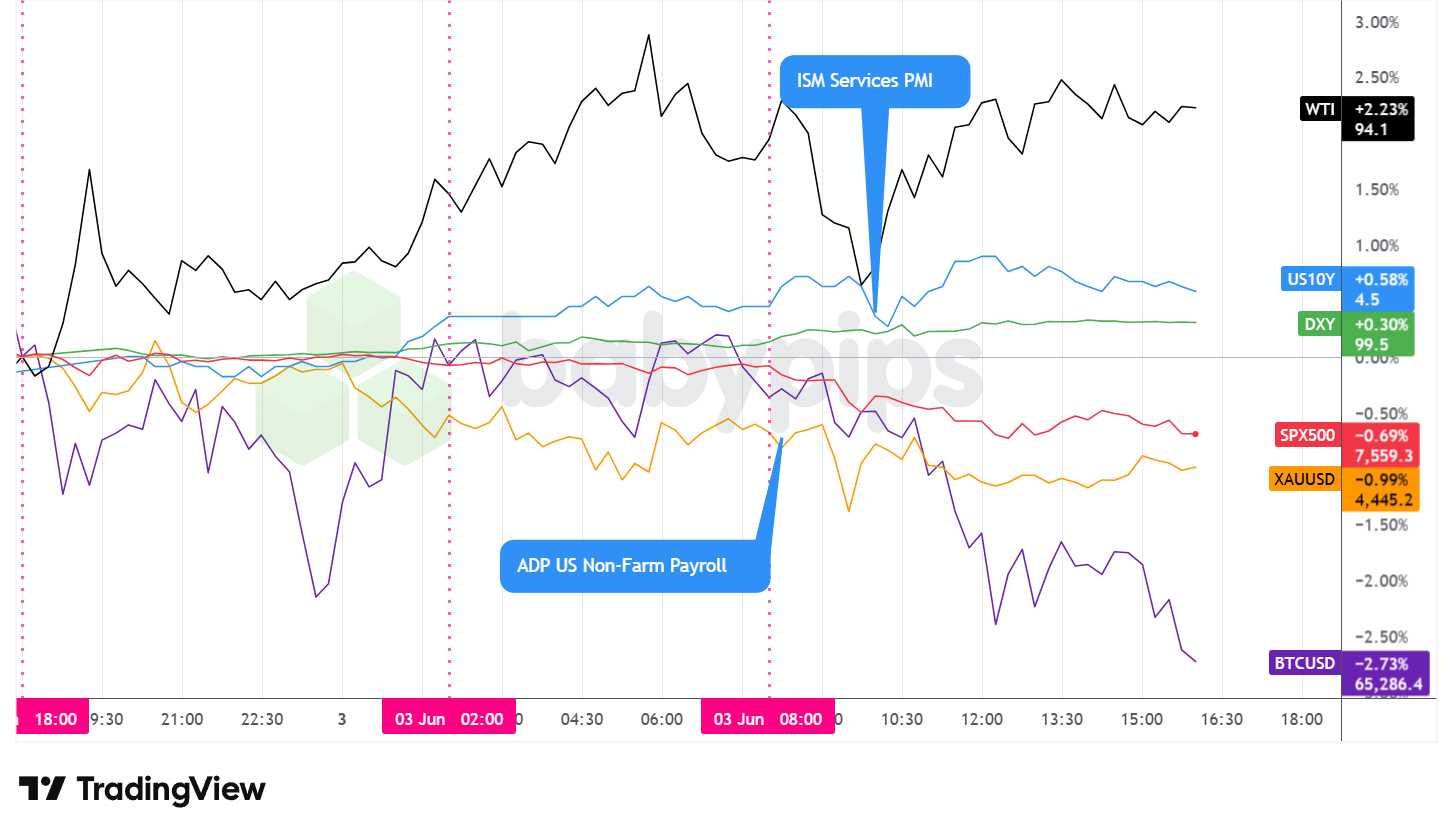

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

Wednesday’s session played out along two competing fault lines: a geopolitical risk premium driven by US-Iran military exchanges across the Gulf, and a hawkish Federal Reserve repricing fueled by stronger-than-expected US economic data. In broad terms, crude oil surged while equities retreated from record highs, precious metals declined despite the conflict backdrop, and Treasury yields moved higher.

WTI crude oil was the session’s strongest performer, rising approximately 2.23% to settle near $94.10 per barrel. The advance began in the Asian session, coinciding with reports of Iranian ballistic missile strikes on US military installations in Kuwait and subsequent strikes extending to Bahrain, Saudi Arabia, and Dubai. The overnight escalation injected a significant supply-risk premium into energy markets, with prices climbing sharply before consolidating at elevated levels through the US session. A larger-than-expected EIA crude inventory drawdown of nearly 8 million barrels, well above the prior week’s draw, may have provided additional support near the close.

The S&P 500 snapped a nine-session winning streak, declining approximately 0.69% to close near 7,559. The index traded broadly sideways through the overnight and early European hours before selling pressure built following the ADP employment report, which came in well above expectations. Losses appeared to extend further after the ISM Services PMI and its associated sub-indexes printed substantially ahead of forecasts, which the market may have interpreted as reinforcing the case for a higher-for-longer rate environment. Reports indicated a software-sector ETF fell more than 4% on the day, with technology shares among the harder-hit groups amid the broader risk-off tone.

Gold declined approximately 0.99% to close near $4,445, a somewhat counterintuitive result given the intensity of the geopolitical backdrop. Gold was steady during the Asian session before trending steadily lower through the European and US hours. The decline appeared to coincide most closely with the strong US data releases, possibly reflecting a hawkish repricing of real yield expectations that outweighed the typical safe-haven demand the metal tends to attract during periods of geopolitical stress. It is worth noting that gold’s failure to sustain its earlier gains despite active military exchanges in the Gulf suggests the market’s dominant concern on Wednesday may have been the inflation and Fed policy implications of the US economic data rather than the conflict itself.

Bitcoin extended its recent selloff, declining approximately 2.73% to trade near $65,286. The cryptocurrency drifted lower through much of the session, with selling accelerating in the afternoon US hours. No single identifiable catalyst was apparent, so the decline likely reflected ongoing bearish sentiment sparked by Bitcoin ETF outflows and news of the Mt. Gox estate transferred approximately 10,306 BTC from cold storage.

U.S. 10-year Treasury yields rose approximately 0.58% in relative terms, finishing near 4.50%. Yields trended higher through the session and moved most notably around the ADP and ISM Services releases, corroborating the broader hawkish repricing narrative. The direction of the move reinforced signals that bond markets may be reassessing the timeline for any near-term Federal Reserve policy adjustment, with some market commentary noting that persistently strong data is reviving discussion of a potential rate hike rather than a cut.

Have a solid trading strategy but lack the capital? FundedNext empowers disciplined traders by providing simulated trading accounts up to $200K.

Unlike other prop firms, FundedNext imposes no artificial time limits on challenges. You even earn a unique 15% profit share during your evaluation! Once funded, you keep up to a 95% profit split with guaranteed 24-hour payouts. Trade CFDs or Futures your way—even during major news events.

Join over 400K traders who have received $300M+ in payouts. Ready to back your edge?

Learn More About FundedNext! Limited time offer: Use code BPFN for 47% off first 5 Futures FLEX challenges, 40% off of the 6th & beyond. T&C apply.Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

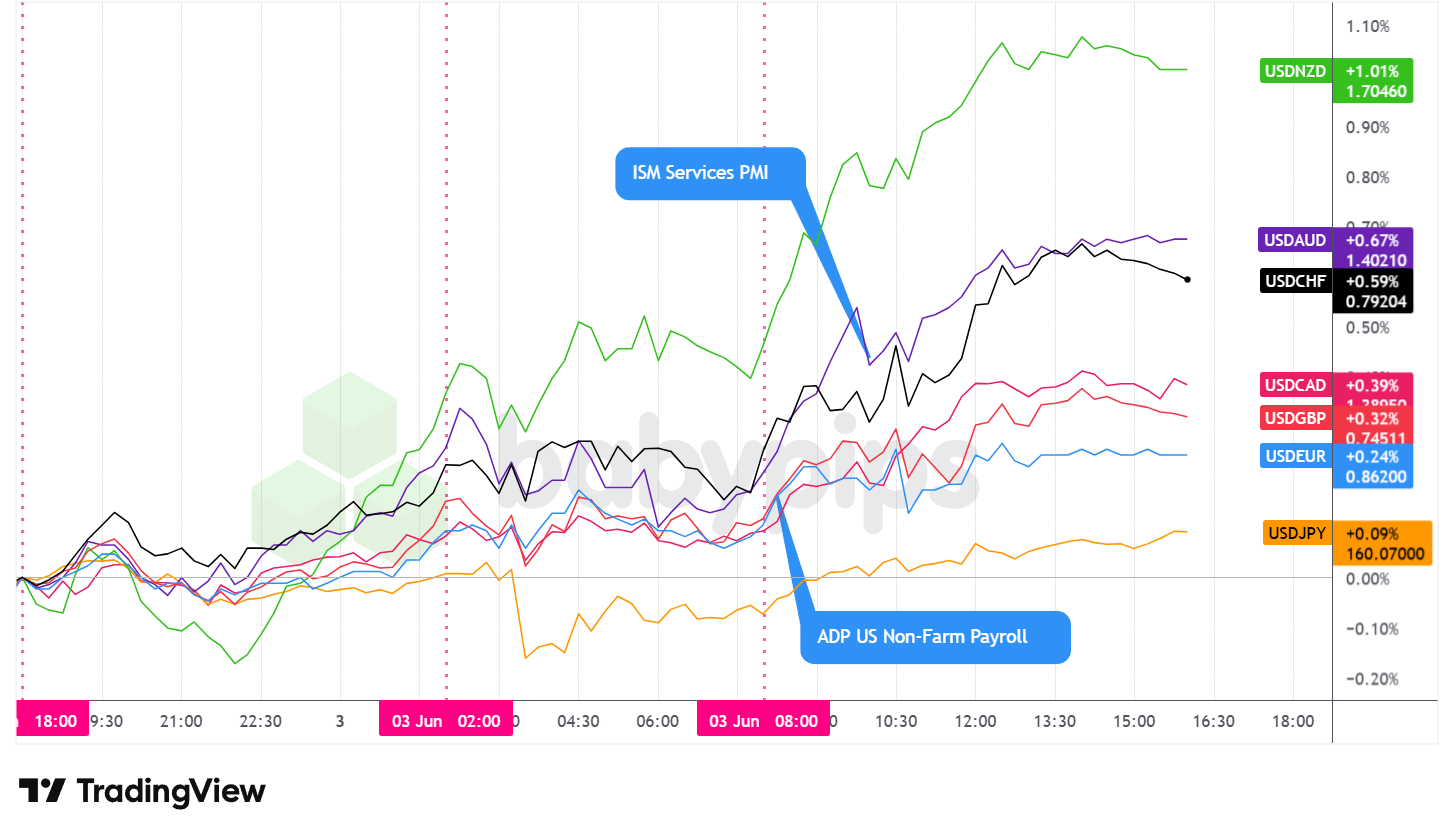

Overlay of USD vs. Majors – Chart Faster With TradingView

The U.S. dollar traded mixed but broadly net higher against major currencies from the Asia open through the end of the US session, closing Wednesday as the best-performing major currency on a daily basis. The DXY finished with a gain of approximately 0.30%, trading near 99.5.

During the Asian session, the dollar drifted net higher against most major peers, though moves were relatively contained in the early hours. The Iranian missile strikes on Gulf military installations provided a potentially supportive backdrop for the greenback, as safe-haven flows during periods of geopolitical stress have historically offered some support for the dollar. A notable development for currency markets was USD/JPY approaching the 160.00 level, the threshold at which Japan spent heavily on currency intervention in 2024. Finance Minister Katayama deployed a verbal warning, stating Tokyo stood ready to respond appropriately as needed. The dollar’s advance in the pair paused near that level as traders grew cautious about pressing the yen further, limiting what might otherwise have been a more pronounced move.

During the London session, the dollar maintained its modest upward lean as European PMI final readings came in above preliminary estimates but remained broadly in contractionary territory. Germany’s services PMI final for May printed at 48.1, beating the 47.8 preliminary figure. The eurozone services PMI final came in at 47.7, above the 46.4 forecast.

The UK’s final services PMI registered 49.3, a meaningful improvement from the 47.9 preliminary reading. Despite the upside revisions, the underlying data still pointed to contraction across much of European services activity, which may have kept modest downside pressure on European currencies relative to the dollar. BOJ Governor Ueda’s reaffirmation of the BoJ’s rate-hiking bias likely offered some restraint on USD/JPY’s advance through this period, one possible explanation for the yen’s relative resilience compared with other major counterparts.

During the U.S. session, the dollar’s upward momentum became more pronounced as a sequence of strong domestic data releases broadened the performance gap between the US economy and its peers. The ADP National Employment Report showed private-sector payrolls increased by 122k in May, well above the 75k consensus and the strongest reading since January 2025.

The ISM Services PMI followed, printing at 54.5 against a 53.0 forecast, with new orders surging to 57.3 and business activity reaching 57.7. Factory orders also came in significantly above expectations, rising 4.8% month-on-month. The collective strength of the US data reinforced a narrative of resilient economic momentum alongside persistently elevated service prices, which appeared to drive a hawkish reassessment of Federal Reserve policy expectations and extended the dollar’s gains against most major counterparts. The Fed Beige Book, released later in the session, noted broadly stable employment and rising inflation driven by elevated energy costs, adding further weight to the picture of economic resilience.

Promoted: The Strategy is Half the Battle; Your Mindset is the Rest.

In “Unknown Market Wizards,” (⭐ 4.6★ | 1,400+ reviews on Amazon) Jack Schwager interviews successful traders to reveal a common truth: their edge isn’t just knowledge or skills—it’s their psychological resilience and rigid risk control. Whether you’re navigating shifting geopolitical themes or top tier economic data, learn how the “wizards” stay clinical when the rest of the market is emotional.

Master Your Trading Mindset with Market Wizards!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- Australia Balance of Trade for April 2026 at 1:30 am GMT

- Australia RBA Gov Bullock Speech at 5:00 am GMT

- Australia RBA Kent Speech at 5:00 am GMT

- Swiss Inflation Rate for May 2026 at 6:30 am GMT

- Swiss Unemployment Rate for May 2026 at 7:00 am GMT

- European Central Bank President Lagarde Speech at 8:00 am GMT

- U.K. New Car Sales for May 2026 at 8:00 am GMT

- Euro area Retail Sales for April 2026 at 9:00 am GMT

- U.S. Challenger Job Cuts for May 2026 at 9:30 am GMT

- U.S. Nonfarm Productivity Final for March 31, 2026 at 12:30 pm GMT

- U.S. Unit Labor Costs for March 31, 2026 at 12:30 pm GMT

- U.S. Fed Barkin Speech at 12:30 pm GMT

- U.S. Initial Jobless Claims for May 30, 2026 at 12:30 pm GMT

- Bank of England Gov Bailey Speech at 3:40 pm GMT

- U.S. Fed Daly Speech at 5:10 pm GMT

Thursday’s calendar is anchored by the US labor market data cluster at 12:30 pm GMT. Initial Jobless Claims for the week ending May 30 arrive one day ahead of Friday’s Nonfarm Payrolls report, making them an early indicator of whether the labor market resilience suggested by Wednesday’s ADP beat is extending into the new month. Nonfarm Productivity and Unit Labor Costs for Q1 2026 release at the same time, potentially adding nuance to the inflation and labor cost picture that markets spent much of Wednesday repricing around. Fed Governor Barkin’s speech at the same hour will draw particular attention, as any commentary addressing the threshold for a policy shift could move the dollar and Treasury market meaningfully given the hawkish repricing already underway.

In the European session, ECB President Lagarde’s speech at 8:00 am GMT will be watched for her assessment of inflation risk in the context of the ongoing Middle East conflict, following ECB Executive Board member Elderson’s comments Wednesday that a prolonged war raises the likelihood of second-round effects. Euro area Retail Sales for April at 9:00 am GMT will add to the data picture of European consumer health, relevant context ahead of any ECB policy signal. BoE Governor Bailey’s speech at 3:40 pm GMT will be monitored for any shift in the Bank of England’s tone given the elevated inflation backdrop.

For Australian dollar traders, RBA Governor Bullock and RBA Kent speak at 5:00 am GMT in the wake of Wednesday’s softer Q1 GDP print, and their remarks will be parsed for any recalibration of the RBA’s growth or rate outlook. The Australian Trade Balance for April at 1:30 am GMT will offer an early look at external sector conditions ahead of those appearances.

Stay frosty out there, forex friends!

Wednesday’s market saw conflicting signals: geopolitical risk in the Gulf, yet gold fell. Strong US data, yet equities sold off. Oil surged while precious metals declined. Understanding why assets moved the way they did requires more than watching one chart at a time. Premium members can read our lesson:

📖 What Is Intermarket Analysis?

Reading this helps you understand how asset classes connect to each other, why gold’s failure to sustain gains despite conflict reveals the market’s true concern, and how the relationship between oil, bonds, equities, and currencies tells you what traders are actually worried about.

And if you’re not a Premium subscriber yet, now is a good time to join.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand the hidden relationships between markets, so you’re reading what the market actually cares about rather than just reacting to headlines.