Tech-led gains drove U.S. equities to fresh all-time highs on Wednesday, while a blowout April PPI print and Kevin Warsh’s Fed Chair confirmation reinforced higher-for-longer rate expectations. Nvidia, Tesla, and Apple executives joined President Trump’s business delegation to Beijing, lifting megacap technology shares even as data showed wholesale producer prices accelerating to 6.0% year-over-year in April. The U.S. dollar closed net higher against most major peers, gold and oil retreated, and a $25 billion 30-year Treasury auction saw investors accepting yields approaching 5% for the first time since 2007.

Check out the forex news and economic updates you may have missed in the latest trading session!

Forex News Headlines & Data:

- Japan Current Account for March 2026: 4,682.0B (3,885.0B forecast; 3,933.0B previous)

- Japan Bank Lending for April 2026: 5.4% y/y (5.0% y/y forecast; 4.8% y/y previous)

- Australia Wage Price Index for Q1 2026: 3.3% y/y (3.3% y/y forecast; 3.4% y/y previous); 0.8% q/q (0.8% q/q forecast; 0.8% q/q previous)

- New Zealand Business Inflation Expectations for Q2 2026: 2.53% (1.7% forecast; 2.37% previous)

- Japan Eco Watchers Survey Outlook for April 2026: 39.4 (36.0 forecast; 38.7 previous)

- Euro area Employment Change Prel for Q1 2026: 0.5% y/y (0.6% y/y forecast; 0.7% y/y previous)

- Euro area GDP Growth Rate 2nd Est for Q1 2026: 0.8% y/y (0.8% y/y forecast; 1.2% y/y previous)

- Euro area Industrial Production for March 2026: 0.2% m/m (0.5% m/m forecast; 0.4% m/m previous); -2.1% y/y (-1.4% y/y forecast; -0.6% y/y previous)

- U.S. MBA 30-Year Mortgage Rate for May 8, 2026: 6.46% (6.45% previous)

- U.S. MBA Mortgage Applications for May 8, 2026: 1.7% (-4.4% previous)

- Germany Current Account for March 2026: 23.6B (18.4B forecast; 22.0B previous)

- U.S. PPI for April 2026: 6.0% y/y (4.7% y/y forecast; 4.0% y/y previous)

- U.S. Core PPI for April 2026: 5.2% y/y (4.1% y/y forecast; 3.8% y/y previous)

- U.S. EIA Crude Oil Stocks Change for May 8, 2026: -4.31M (-2.31M previous)

- On Wednesday, Federal Reserve Bank of Boston President Susan Collins argued that interest rates should remain steady for “some time” due to concerns that persistent inflation and Middle East conflict risks may require a prolonged restrictive monetary policy.

- Bank of Canada Summary of Deliberations: Officials expressed a “range of views” regarding the future path of interest rates, indicating they may need to be nimble as they weigh the competing economic risks of potential U.S. trade tariffs against inflationary pressures from the conflict in the Middle East.

- The U.S. Senate confirmed Kevin Warsh as the next Federal Reserve Chair by a 54-45 vote, the slimmest margin in the central bank’s history, announced at approximately 2:47 PM ET. Warsh is set to replace Jerome Powell, whose term as chair ends Friday. Warsh vowed during his confirmation hearing that Fed monetary policy would remain “strictly independent,” though President Trump has publicly called for immediate rate reductions.

Promoted: Day traders & Scalpers have better odds of making great decisions if they see market catalysts right away. Get the real-time feed that pros use to catch the news.

Join FinancialJuice for Free to learn more!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Broad Market Price Action:

{kind=link}

Dollar Index, Gold, Oil, S&P 500, U.S. 10-yr Yield, Bitcoin Overlay – Chart Faster With TradingView

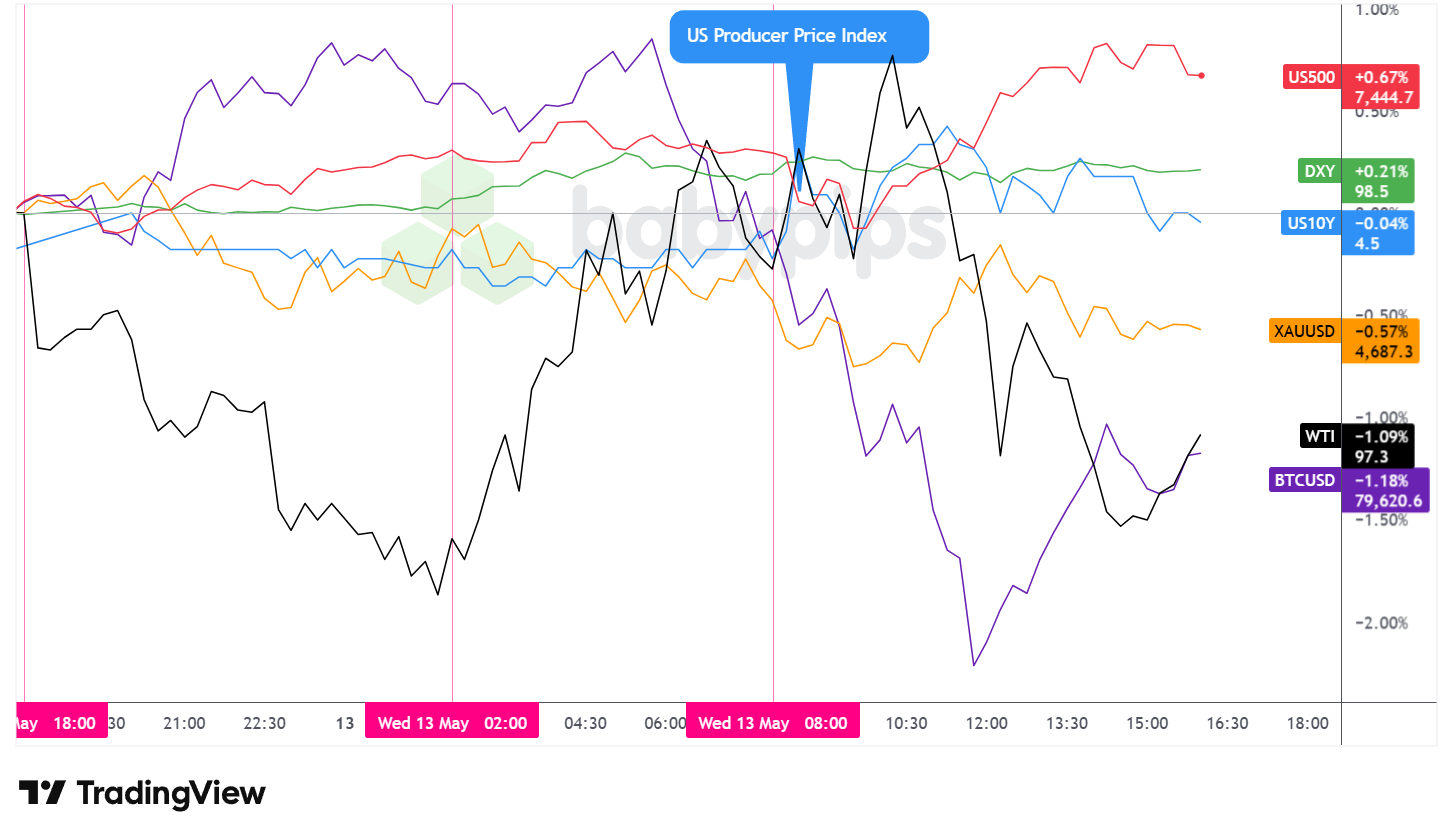

Wednesday’s broad market session produced a striking divergence: U.S. equities surged to record highs on the back of technology megacap enthusiasm, while inflation-sensitive assets pulled back and bond markets absorbed the hottest wholesale price data since 2022. The common thread running through the session was the April Producer Price Index, which came in dramatically above expectations and set the tone for cross-asset positioning well into the afternoon.

The S&P 500 rose approximately 0.67% to close near 7,444.7, notching another fresh all-time high. The intraday path was more volatile than the headline gain suggests. Futures drifted gradually higher through the Asian session and into early London trade, reaching the 7,430 area before the U.S. open. The PPI release triggered a sharp pullback toward the 7,375 area, but the index quickly reversed and rallied to a session high near 7,460 before trimming slightly into the close. The spark behind the strength appeared to be the symbolic and commercial weight of Trump’s Beijing delegation: Nvidia’s Jensen Huang, along with the chief executives of Tesla and Apple, were confirmed to be traveling with the president to China, a development that likely reinforced investor optimism around the near-term technology and trade outlook.

Gold declined approximately 0.57% to close near $4,687.3 per ounce. The precious metal entered Wednesday already under modest pressure, edging lower from the prior session through the Asian hours. A tentative recovery attempt during the early London session faded, and the PPI release appeared to extend the selling, with gold briefly testing below the $4,670 area before stabilizing and partially recovering into the close. A firmer U.S. dollar likely weighed on bullion at the margin, though gold’s relative resilience above $4,670 despite the sharp inflation surprise may suggest some underlying demand remains present in the current geopolitical environment.

WTI crude oil fell approximately 1.09% to close near $97.3 per barrel. The commodity spent the Asian session sliding from just below $98 toward the $96.5 area, before staging a recovery rally through London trade to a session high near $99.25. That recovery gave way during U.S. hours, with oil gradually retreating to close near the day’s lows. The EIA crude inventory report showing a drawdown of 4.31 million barrels for the week ending May 8 provided a modest counterbalance to the bearish price action, though the data was not enough to sustain the earlier recovery. The broader backdrop of an unresolved Strait of Hormuz disruption continues to anchor oil above the $95 area.

Bitcoin fell approximately 1.18% to close near $79,620.6. The cryptocurrency followed a notably different intraday path from equities, climbing to a session high near $81,286 during the Asian session before reversing sharply through London and early U.S. trading hours, shedding more than $2,500 from peak to trough and touching a session low near $78,715. A partial recovery followed through the afternoon. With no apparent direct catalysts for the reversal, the decline may have reflected profit-taking following the prior session’s strength, or some broader reassessment of risk appetite as the inflation implications of the PPI data became clearer.

The U.S. 10-year Treasury yield finished little changed, edging down approximately 0.04% to close near 4.50%. Intraday, yields were more volatile: the PPI release triggered an initial spike toward the 4.494 area, only for yields to retrace in subsequent hours. Despite the surface-level stability in the 10-year, the session’s $25 billion 30-year bond auction saw investors accepting 5% yields on those maturities, the highest since 2007, suggesting bond markets are pricing in an extended period of elevated rates regardless of near-term 10-year movements.

Promotion: If your confidence has grown in your market awareness & strategies with this market recap, and you wanna take action, Maven Trading can help. They provide simulated funding challenges starting as low as $15, allowing you to trade major pairs with professional-sized capital. No time limits mean you can take swing plays on these market themes without the pressure of a ticking clock.

Learn More About Maven Trading Today!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Majors – Chart Faster With TradingView

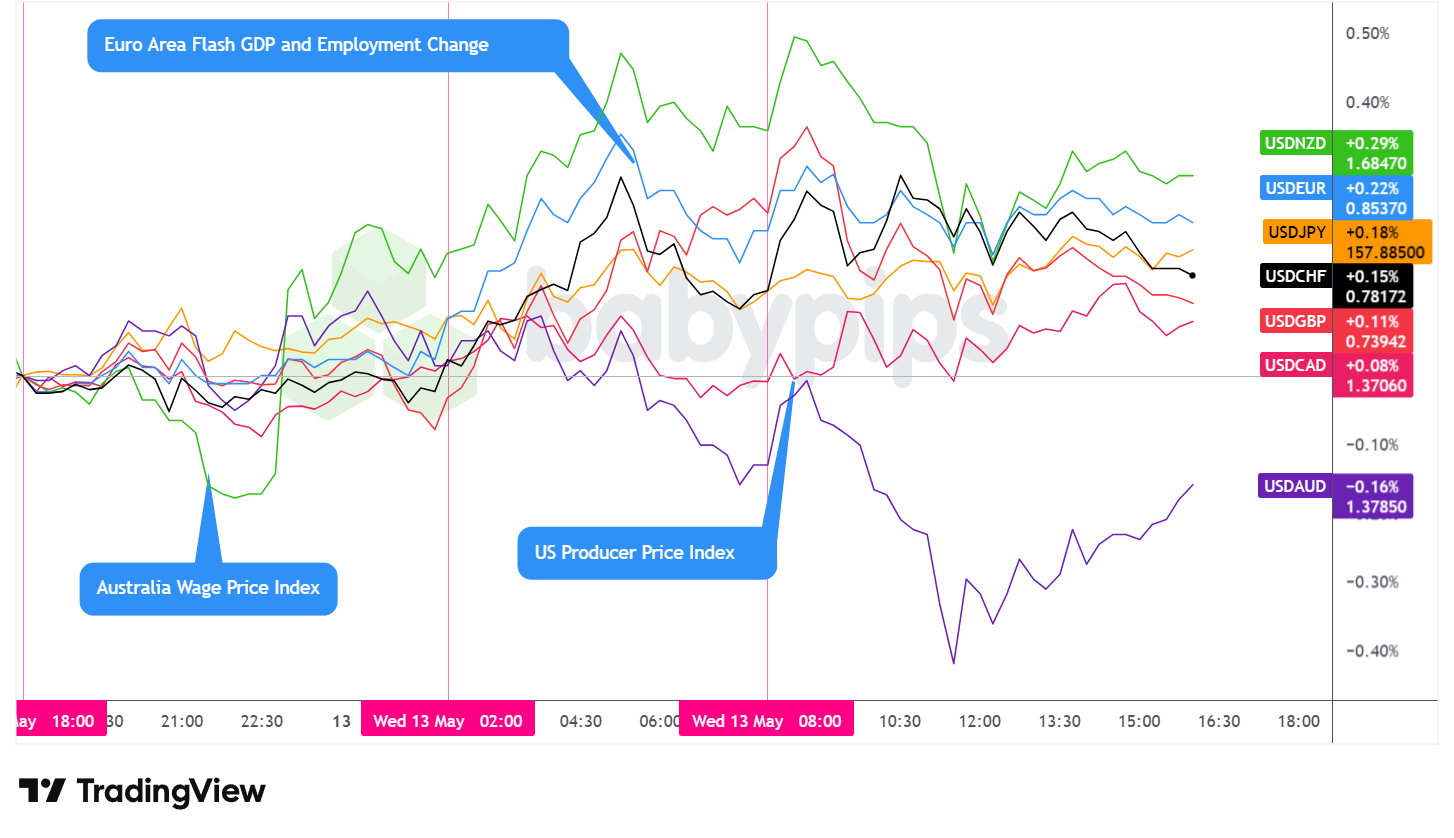

The U.S. dollar closed Wednesday as one of the session’s best-performing major currencies, finishing net higher against all major peers with the sole exception of the Australian dollar, in a session that played out across three fairly distinct phases.

During the Asian session, the dollar traded with a net bullish lean, edging gradually higher across most pairs from the overnight open. The session’s regional data flow was active without being definitive for the dollar itself. New Zealand’s Q2 2026 Business Inflation Expectations came in sharply above the forecast at 2.53% versus 1.7% expected and above the prior 2.37%, which may have contributed to NZD underperformance on the day. Australia’s Q1 Wage Price Index printed at 3.3% y/y, exactly in line with the forecast and a slight deceleration from the prior 3.4%. However, the accompanying housing finance data missed badly on both the investment lending and owner-occupier measures. The dollar continued its net bullish drift against the other major currencies through the mid-morning London session before pulling back modestly ahead of the U.S. session open.

During the London session, the focus shifted to European data. The Eurozone’s Q1 2026 GDP second estimate was confirmed at 0.1% q/q and 0.8% y/y, matching the preliminary reading but representing a marked deceleration from the 0.2% q/q and 1.2% y/y recorded in the prior period. Employment growth also slowed. German wholesale prices for April came in hotter than expected at 6.3% y/y against a 5.2% forecast, consistent with the broader pattern of energy and commodity cost pressures working their way through supply chains. France’s final April CPI was confirmed at 2.2% y/y, up from 1.7% previously. ECB commentary added a cautious tone, with multiple officials noting the need for more information before June’s decision, and one suggesting a fast resolution to the Strait of Hormuz crisis would be needed for the ECB to hold rates at current levels. The dollar maintained its net bullish posture through this session, though the pace of gains moderated across most pairs.

During the U.S. session, the dollar initially extended its advance after the session opened, but turned lower shortly ahead of the U.S. equities open and then ground slowly lower through the remainder of the session. The April PPI release showed headline producer prices rising 6.0% y/y against a 4.7% forecast, with the monthly advance of 1.4% the sharpest since 2022. Core PPI accelerated to 5.2% y/y, the highest in more than three years, and even the ex-food, energy, and trade measure came in at 4.4% y/y against a 3.7% forecast, suggesting the inflationary impulse is broader than energy alone. Despite the initially bullish tone that such a data print might suggest for the dollar, the greenback subsequently reversed and drifted lower for much of the afternoon. One possible interpretation is that markets were already expecting a hot number, as signaled by the runup leading to the data release and yesterday’s CPI data, and took profit when the news was confirmed. The Senate confirmation of Kevin Warsh as Fed Chair, announced at 2:47 PM ET, added another layer of uncertainty around the Fed’s near-term policy trajectory.

Promotion: When the Market Swings, Are You Reacting or Executing?

In “Positive Trading Psychology,” renowned psychologist Brett Steenbarger reveals in his newest book that the secret to navigating volatility isn’t “fixing” your flaws—it’s doubling down on your innate character strengths. Learn how to stay clinical while the rest of the market is emotional, turning sudden market shaking news into your professional edge.

Learn more about “Positive Trading Psychology: Turning personal strengths into trading strengths” on Amazon!

Disclosure: We may earn a commission from our partners if you sign up through our links, at no extra cost to you.

Upcoming Potential Catalysts on the Economic Calendar

- New Zealand Visitor Arrivals for March 2026 at 10:45 pm GMT

- U.S. Fed Logan Speech at 11:00 pm GMT

- U.K. RICS House Price Balance for April 2026 at 11:01 pm GMT

- China President Trump and President Xi Summit

- Australia Consumer Inflation Expectations for May 2026 at 1:00 am GMT

-

U.K. GDP for March 2026 at 6:00 am GMT

- U.K. Manufacturing & Industrial Production for March 2026 at 6:00 am GMT

- U.K. Balance of Trade for March 2026 at 6:00 am GMT

- China Monetary Developments for April 2026

- ECB President Lagarde Speech at 9:15 am GMT

- U.K. NIESR Monthly GDP Tracker for April 2026 at 11:00 am GMT

- Canada New Motor Vehicle Sales for March 2026 at 12:30 pm GMT

- Canada Wholesale Sales Final for March 2026 at 12:30 pm GMT

- U.S. Retail Sales for April 2026 at 12:30 pm GMT

- U.S. Import & Export Prices for April 2026 at 12:30 pm GMT

- U.S. Initial Jobless Claims for May 9, 2026 at 12:30 pm GMT

- U.S. Fed Hammack Speech at 5:00 pm GMT

Thursday’s most closely watched release will likely be U.S. retail sales for April at 12:30 pm GMT, arriving in the immediate aftermath of back-to-back inflation surprises in CPI and PPI. A soft consumption reading alongside the week’s hot inflation data could reinforce stagflation concerns that are already creeping into market commentary, while a beat might suggest consumer demand remains resilient enough to sustain an extended Fed hold. Initial jobless claims will offer a concurrent read on labor market conditions.

In the London session, a dense block of U.K. data at 6:00 am GMT, including GDP, manufacturing and industrial production, and the trade balance for March, will be watched closely against the backdrop of persistent energy-driven inflation. ECB President Lagarde’s speech at 9:15 am GMT may draw particular attention after Wednesday’s mixed ECB commentary around June’s decision and the unresolved Hormuz situation.

The Trump-Xi summit in Beijing continues and remains the session’s most unpredictable wildcard. Any substantive announcements on technology trade, tariffs, or Hormuz-adjacent diplomatic positioning could move multiple asset classes simultaneously across the Asian and European opens.

Stay frosty out there, forex friends!

Wednesday’s market session showcased a textbook risk-on/risk-off split: equities surging to record highs while inflation-sensitive assets retreated, but you may not realize how deeply this mood shift flows through forex markets and currency valuations. Premium members can read our lesson:

📖 Risk-On / Risk-Off: How Global Mood Moves Currencies

Reading this helps you understand how market appetite for risk drives currency flows, which currencies strengthen when traders feel bold versus scared, and how to check the risk environment before placing any trade.

And if you’re not a Premium subscriber yet, now’s a good time to sign up.

With Babypips Premium, you get full access to School of Pipsology lessons that help you understand not just which currencies rally when risk appetite shifts, but the geopolitical and inflation dynamics that trigger the shift in the first place